This last month marked my one year anniversary of using the app, You Need a Budget, or YNAB, and to say I’ve been dying to share my progress is an understatement.

I figured YNAB would be one of those things to pass the time while stuck at home during the pandemic. At the very least it’d be something to do during the couple weeks I’d be stuck at home. Little did I know, I’d still be here a year later, and little did I know much YNAB would change my finances during that time.

I want to start out by saying I’ve been incredibly lucky to not only keep my job during this past year, but also by being able to work from home this whole time. I truly feel for those who didn’t share my situation.

Regardless of what my situation had been, finding YNAB at the start of the pandemic couldn’t have been better timing. The world was facing the uncertainty of a pandemic, and I was almost $9000 in debt with basically nothing in the bank.

Creating a Plan

My first month of using YNAB was all about creating a plan. It turns out despite using Mint for all these years, I really had no clue what to do with my money. If there was more than $1000 in the bank, I figured it was safe to spend, so I did. Instead, I had a great idea of where my money went in the form of nagging “overspending” alerts, which weren’t all that helpful after I’d spent my money. YNAB flipped Mint’s budgeting model on its head and forced me to create a plan for every dollar (rule 1) before I spent it.

Paying Off Credit Cards

My second month of using YNAB ended up being one of those rare months full of unexpected money (why can’t they all be like that!) – a 3 paycheck month, tax refunds, and a stimulus check. In the past, I would have squandered this extra money on random things from Amazon, but armed with my plan, I put the extra money to work for me towards the goals I had set out.

My first goal was to pay off my credit cards, which I’d been unsuccessful at doing pretty much ever since I got the cards. Thankfully, I never wracked up tons of credit debt, but I always seemed to have some combination of around $2000-4000.

Thanks to the extra income in April, I was able to pay off all three of my credit cards. My initial goal was to pay off 1 card by the end of 2020. I’m also happy to say that thanks to the way YNAB forces you to treat credit cards as if they’re debit cards, I’ve continued to completely pay off my cards each month ever since. Getting paid to use a credit card is a lot better than paying interest.

Paying Off the Car

My second goal was paying off my car. Pre-YNAB this seemed like a goal I’d be able to tackle by December 2021 at the earliest, but I ended up doing it in August of 2020. This was actually an even bigger deal to me because I actually accomplished another goal, of becoming debt-free other than the mortgage by the time I celebrated my 30th birthday which I hadn’t even imagined being possible 2 months prior.

Feeling YNAB Broke

One of the reasons I was consistently over budget using Mint was that I wasn’t planning for what YNAB considers True Expenses (rule 2) – things like that yearly Amazon Prime subscription, a new set of tires, or the appliance that inevitably gives out at the worst time. Every month one or more of these true expenses would pop up, and because I hadn’t planned for them, I’d pull out the credit card to pay for them.

With YNAB, I started setting aside money for those true expenses. As each one came up, I added it to my budget and started saving a little for it each month. Eventually I was able to convert a number of my monthly bills to annual plans saving even more money.

As a result, my bank balances started to climb, which is also around the time I started feeling “YNAB Broke” as YNABers like to say. My bank account had more money in it than I’d ever had, but suddenly all those dollars already had jobs. I didn’t have $10,000 in the bank to spend on whatever I wanted. It was already earmarked for car insurance or Christmas gifts.

As time went on, I stopped noticing my bank balances altogether. Category balances are what I check, and since they rarely have more than a few hundred dollars in them, you feel broke even though you have more money.

Getting a Month Ahead

One of YNAB’s other tenants is to try and break the paycheck to paycheck cycle by getting a month ahead (or in other words, using last month’s income to pay this month’s bills). It’s rule 4 and they call it aging your money.

This was one of those things that seemed a bit overblown to me but turned out to be unexpectedly rewarding. Each month as my debts went down and more of my true expenses were accounted for, paychecks seemed to get me funded a little further down the budget until one day I realized the whole month was funded and I was still expecting another paycheck for the month. It seems simple, but starting the month knowing everything is accounted for has added so much peace of mind to my life.

Building My Emergency Fund

After getting a month ahead, I refocused my sights on my emergency fund. I had saved up $1000 (Dave Ramsey’s Baby Step 1), but my eventual goal is to have 6 months worth of expenses. I currently have around 2 months of expenses saved for this. Paired with being a month ahead and saving for true expenses, I consider this really a 3 month emergency fund, which brings us to today.

My Goals for 2021

Finally feeling secure in my finances for the first time in my life, I pushed pause on increasing my 3 month emergency fund to 6, and set my sights on the future.

I recently opened a Roth IRA with M1 Finance, and pressed paused on the emergency fund because I wanted to max out my Roth IRA for 2020 and knew I only had until April to do this. (The IRS has since extended the deadline to May.) As of this past March, I’ve reached my goal. Going forward, I’ve built monthly contributions of $500 into my budget so that so I won’t need to play catch up to max out my contributions for years going forward.

My other goals for the rest of the year, all of which I’m on track to complete, are as follows:

- Finish saving for our wedding

- Refinance our condo to a 15 year mortgage

- Complete saving a full 6 months worth of expenses in case of an emergency

Looking Back

Prior to finding YNAB, I assumed I just didn’t make enough money and my financial situation doomed unless I got another job. I felt stuck with no way up. It turns out my income wasn’t the problem. It was my behavior.

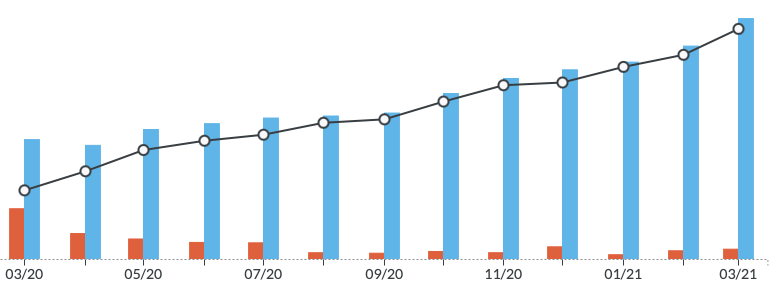

In just one year, I went from living paycheck to paycheck and $9000 in debt to being debt free. The net worth graph from the past year says it all.

My friends and family think I’m a bit YNAB-obsessed, and truthfully I am constantly singing its praises. I’ve definitely drank the Kool-aid, but honestly, if you’d shown me this graph a year ago and told me it would be mine today, I wouldn’t have believed you. Trying YNAB has truly been one of the best decisions I’ve made and if this is the progress I made in one year, I can’t wait to see what’s in store for the future.

And if you want to try YNAB for yourself, the links to it included on this page will get us both an extra free month if you choose to sign up after the 34 day free trial. Did I mention there’s no credit card required to sign up, so it’s totally risk free. They aren’t some sketchy company that will immediately sign you up at the end of the trial.

Onwards and upwards.