I’ve written in the past about my keyboard shortcuts for quick entry on my Mac. At this point using ⌘+space to launch Alfred, ⌥+space for quick entry for Things, and ^+space to jot down notes have become muscle memory.

While the app has changed a few times over the years, Drafts was my app of choice for jotting notes the longest. I mean its tag line is literally, “Where text starts,” and it’s honestly great at it. But in the back of my mind, I always felt like I just wasn’t using Drafts to its full potential, and with that nagging at me, I found myself tinkering and trying to optimize the app over and over again. I set up actions and action groups, organized my workspaces, played with themes, and hid as much as I could to make the app as minimal as possible. No matter what I did, I’d find myself myself back to jotting down notes in one jumbled workspace, and when I needed to get text out of Drafts, I wasn’t using any of the actions I created. I was using MacOS’s built in Share extension, and most of the time, the app I was sharing things to was Apple Notes. Drafts was overkill for my needs and really just serving as another junk drawer for notes, and so I kept asking myself, “Why create notes in Drafts when I could just create them in Apple Notes to begin with?”

When Apple released the Quick Note feature for MacOS with Monterey, I saw this as my chance to see if I could get away with using Apple Notes and the Quick Note feature to replace Drafts entirely.

Two years later, I think it’s safe to say I can.

By default, Apple sets up Quick Note to be triggered via a hot corner, but I already use my hot corners for other things. What I really wanted was to be able to trigger it via ^+space like I was used to with Drafts. Apple doesn’t make it easy to set up a keyboard shortcut for the Quick Note feature. It’s definitely not in Apple Notes settings where it should be, but it is possible.

To set up a keyboard shortcut for it, go into System Settings > Keyboard > Keyboard Shortcuts > Mission Control. There you should find an option for Quick Note to add the shortcut of your choosing.

Apple’s Quick Note window turns out to be the minimal, quick note taking solution I was looking for (no pun intended). On top of that, anything I jot down gets saved into Apple Notes automatically, so I don’t need to worry about sharing it to Apple Notes. I can also share it out to other apps if I need to using the share extension, and because I already review Apple Notes every week as part of my weekly review, that’s also one less inbox I need to review every week.

If you’ve wanted to use something like Drafts for quick text entry, but felt it was overwhelming, I highly recommend seeing if Apple Notes can fit your needs. It certainly fit the bill for me.

Long-time readers may recall that about a year ago I actually said I wasn’t a fan of time blocking because I hated planning out my days in excruciating detail. Yet, here I am today about to tell you how I’m tracking my time.

I’ve read countless books that recommend tracking your time. I’ve never doubted that it’s a valuable exercise. That being said, I’m also lazy, so I’ve avoided doing it because, “Ain’t nobody got time for that!”

In the world of customer support, my days are pretty reactionary. My core work is providing support for the projects others have rolled out. Most of my time doesn’t fit neatly into deliverables, milestones, and deadlines, but is instead reserved for being available and ready to help someone in the event things happen to go wrong.

The project I’m currently working on, however, does fit neatly into deliverables and deadlines, and the people I’m working with on it are used to tracking their time to make sure they hit their milestones. We’ve also been given a particularly ambitious go live date for this particular project. Not only was I not about to oppose how my colleagues usually do things, but I also saw the value in being able to document how much time I’m spending on this project, and equally as important, why I’m not spending more time on it as a way to manage expectations around a realistic scope and timeline.

I’m also not one to do something half way, so if I was going to be tracking time for this project, I might as well track the rest of my time too.

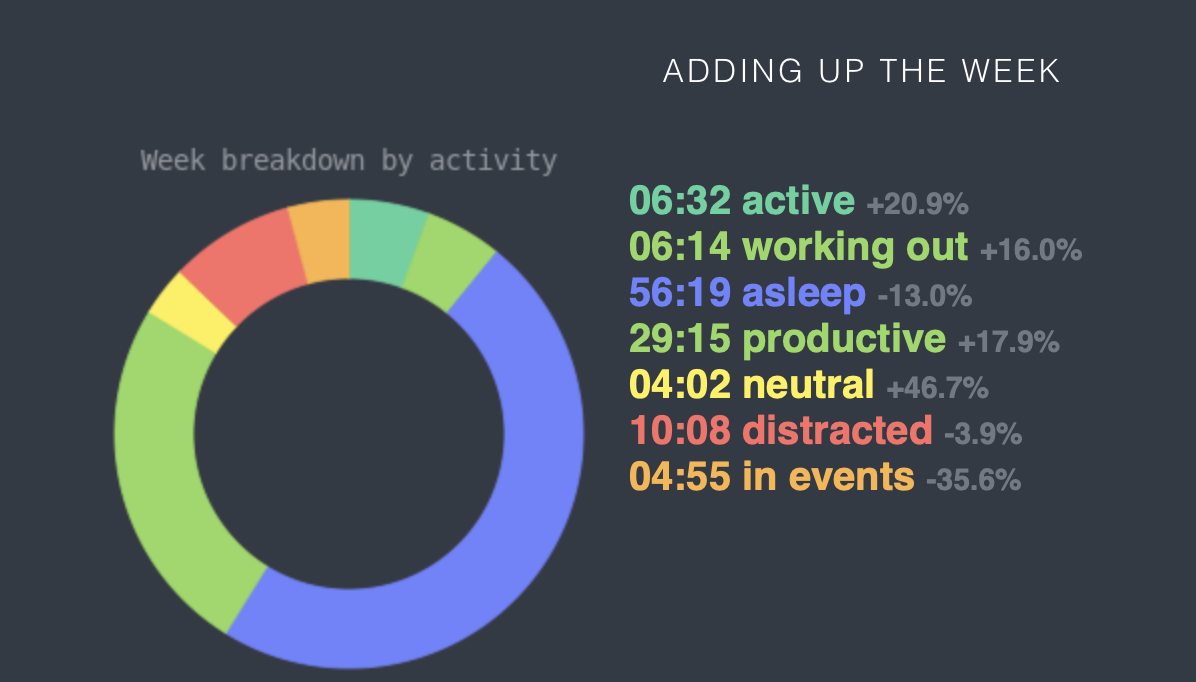

I settled on using Toggl. It’s free, highly recommended, and also syncs with Exist.io which I’ve been using for years (albeit with a brief hiatus) to discover trends in health, activity, and other aspects of my life. The Mac and iOS apps for Toggle do what you’d expect, and I also appreciate that they include a Pomodoro function. More on that in a bit.

Because Exist considers time tracked in Toggl productive time, I settled on tracking the time I spend on things on my Today list in Things, with the exception of workouts. While I definitely consider working out as productive time, Exist already tracks working out via Apple Health. Tracking it with both Toggl and Apple Health effectively double counts it in the weekly summary report it sends out which I don’t want.

I also track a few things that aren’t on my list, like the amount of time I spend providing customer support. Because I don’t know when a customer is going to reach out with a question those tasks generally aren’t part of my daily task list.

After tracking my time for a little over a month, I have noticed a few benefits:

I’m more productive than I thought. It may be shocking to readers to know that I don’t feel a productive person. Like I said earlier, I’m admittedly quite lazy. The systems I use in my daily life are there so that I can work through my to do list as quickly as possible because I want to be able to do absolutely nothing for the rest of the day. Tracking my time showed me I’m more productive than I was giving my credit for. It’s hard to argue with actual data.

I batch my tasks more. Again with the laziness, constantly starting and stopping timers in Toggl got old quickly. Not only was I forgetting to start and stop timers, I didn’t like seeing my day broken up into tons of little time blocks. As a result, I started batching my tasks so that I could set one timer and work through multiple related tasks at once.

I’m less distracted. By now we know multitasking doesn’t work. Batching my tasks already helps with that, but I also find that I’m less likely to switch out of a task to go do something like check my email because I don’t want to stop a timer.

I procrastinate less. For tasks that I feel inclined to defer to another day repeatedly, I’ve been using the Pomodoro function. I tell myself I’ll just work on the task for 20 minutes set the timer and work until it’s done. I’m doing it right now for this blog post. I hadn’t had much success with the Pomodoro method in the past, but combining it with checking something off in my task manager and not wanting to pause or start timers seems to be the the magic combination to making the Pomodoro method work for me.

I get things done faster. Laziness here again, I want to get things done as quickly as possible so I can do nothing, so I try to check of as many tasks as I can within a timer, particularly if I’m using the Pomodoro function. This morning I had a few extra minutes before I had to leave and I had a Chores timer running, so I looked back through my to do list to see if there were any additional chores I could tackle before stopping my timer.

The jury is honestly still out as to whether I will continue tracking my time beyond this project. That being said, after reading all those books that recommend tracking your time, I can now say I’ve actually done it. I can also say it was a worthwhile exercise even if I choose not to continue.

This month marks my three-year anniversary of using You Need a Budget (or YNAB). What started as a way to kill time during the early days of the pandemic has honestly turned out to be one of the best changes I’ve ever made in my life.

I was skeptical about YNAB, a service I’d need to pay, for would help me with my finances. I tracked my finances with Mint for years without much improvement, so clearly the problem wasn’t me or my budget. It had to be my income, and paying for something was the exact opposite of increasing my income.

My finances admittedly could have been worse. I only had a few thousand dollars worth of credit card debt and a car loan, but I was usually one paycheck away from potentially not being able to pay my bills. The thought of losing my home was a constant stress in the back of my mind, and I avoided my finances because of it

I checked my bank accounts as if they were Schrödinger’s boxes. Was there money in them or wasn’t there?

I seemed to always be in a constant cycle of getting hit with “unexpected” expenses (that were actually quite predictable). I’d pay for them with a credit card because I wasn’t sure that I’d have enough money to pay for whatever I was buying and still have money left over for my other bills. When it came time to pay my credit card bill, I’d only pay a portion of my statement balance because, like with my other expenses, I wasn’t sure if I’d have enough money to pay for it and the next round of bills that was coming. I ended up in a revolving cycle of debt I couldn’t seem to get out of.

Mint would tell me the obvious: I was in debt and I’d overspent my budget categories. Like any rational person, I’d vow to do better next month and revise my plan to pay off my debt. Then I’d head over to Amazon to treat myself to that thing on my wishlist that was suddenly 20% off.

My mindset was that if I buried my head in the sand, my financial problems didn’t exist. This cycle of defeat, denial, and impulse spending had been going on for nearly 10 years. To Mint’s credit, it tried to offer me suggestions, but those suggestions were about as effective as telling someone to break up with the person they know is bad for them. They didn’t work for me.

Within days of setting up my budget in YNAB, the problem was obvious.

If Taylor Swift had released Anti-Hero in 2020, I’d have undoubtedly been saying, “It’s me. Hi. I’m the problem. It’s me.”

My problem wasn’t my income. My problem was that I was mentally trying to keep track of my spending in my head:

This puzzle is only $20. $20 isn’t a big deal. I have more than enough in the bank right now to cover $20 and groceries.

I know my car registration is due this month, but I’ll worry about that when I get paid again on Friday.

I can’t decide which craft beer I want, so I’ll just get both six packs today and won’t buy any next weekend.

I know I should get my HVAC system looked at, but I’m not sure if I have enough to pay for it, so I will just hold off.

I was making mental calculations like these constantly, and I was really bad at it:

Sure, that puzzle only cost $20, and I did have enough for groceries, but what about money for anything else?

Yes, I get paid again on Friday, and could use money from that paycheck for my registration, but what if something else comes up?

Let’s be real. I’m probably going to be just as indecisive and want to buy 2 different six packs next weekend. So then what?

I’m going to have to get the HVAC looked at eventually because the problem isn’t going away. I should look up how much it costs and start saving money for it now rather than putting it off indefinitely.

YNAB helped me get the mental spreadsheet out of my head and put it somewhere that I could actually see and use (and if you’ve been following my blog for any amount of time, you know how much a GTD-person like myself loves to get things out of their head).

I spent the first few weeks with my budget open constantly just looking at it. (Side note: If you have any desire to convince others in your house to use YNAB, don’t do this! My friends and family still assume YNAB is super complicated because I spent so much time in my budget.) Seeing my budget meant I no longer had to run the mental calculations in my head. My budget was showing me, “It’s okay. You’ve got this.”

My finances were no longer this mysterious box. Whenever I got money, I planned out exactly how I wanted to use it rather than spending as things happened and hoping for the best at the end of the month.

Thanks to the clarity I got with YNAB, I paid off my credit cards and my car loan in the first 8 months. To this day, I’m debt free other than my mortgage. (Mint suggested I could be debt free by 2024 by the way.) In the past three years, I’ve opened a Roth IRA and max it out each year. I’ve saved 6 months worth of expenses in the event that I lost my job. I also refinanced my mortgage to a 15-year mortgage, keeping my payment the same but cutting the amount of payments in half. Those are just some of the big things.

When I mention how I’ve improved my financial situation, people assume I must have went Dave Ramsey style, living on rice and beans and selling things like my life depended on it, but I didn’t. I spent money on things that mattered and saved on things that didn’t. I actually spent more freely and without guilt about buying things. Every purchase I made was part of my plan, and that plan was no longer focused on just that month or the days until my next paycheck but my future.

I knew I could buy the puzzle because I had $20 in my Fun Money category.

I’d been setting aside a few dollars each month knowing my car registration was due this month. The money was there and waiting for me to pay for it.

I could choose to buy 2 six packs this weekend knowing I’d have less money available for next weekend unless I decided to pull money from elsewhere in my budget.

I researched HVAC companies in my area and have a contract with one, which is in my budget. They call me every spring and fall to arrange a time to come out and look over my system and perform any maintenance needed.

Three years ago, my only financial goal was to get out of debt some day. Quite honestly, it didn’t even seem achievable. YNAB helped me achieve it, but it also fundamentally changed how I think about my finances. My financial goal, now, is to become financially independent and possibly even retire early. I’m excited to see where my finances take me in the future, and once again, a big thank you to YNAB for changing my life.

Disclaimer: This post isn’t sponsored. I just really like YNAB, but if you’re interested in signing up and use my referral link, we’ll both get an extra month free if you choose to subscribe.

And if you’re interested in reading more about my YNAB journey, you can read through my earlier posts.

For those of you that have followed my blog for a while, you know I’ve really wanted to use Apple Notes for my personal knowledge management for a while now. There’s really only one thing holding me back – linking. For reasons unknown to me, Apple seems to have no intention of adding linking any time soon despite it being a feature that’s present in almost every other note taking app.

Even Apple’s other apps like Mail have a way to uncover a link using AppleScript at least. If you want a link to a note in Apple Notes, on the other hand, you have to act as though you’re sharing it with someone via phone or email even if the person you’re sharing it with is just yourself. Oh, and then it adds a wonderful Shared section to Notes to remind you of all the notes you’ve shared with yourself.

My frustration eventually lead me down a rabbit hole that lead to this post – a [very convoluted] way to generate a link to a note without sharing it.

Allow me to introduce how I link to notes in Apple Notes using Keyboard Maestro and Shortcuts.

The Starting Point – Opening an Apple Note with a Shortcut

Theoretically, if you only link to a few notes, you could just create dedicated shortcuts for each note you want to link to and then link to the shortcut using the format shortcuts://run-shortcut?name=Shortcut%20Name. If that sounds good enough for you, you can swap out Clipboard for the actual note title in the following shortcut and call it a day. I, however, like to link to a lot of notes, and I really didn’t want to have to create a new shortcut anytime I wanted to link to a new note.

(By the way, links to everything are included. You’re welcome.)

I started by creating a generic “Open Note” shortcut that opens a note based on your clipboard. This is a simple two-step shortcut:

Find All Notes where Name contains Clipboard

Show Notes

Adding On – Generating a URL Base to Launch the Open Note Shortcut

Like Shortcuts, Keyboard Maestro can launch automations via URL, but it has one super power over Shortcuts’ URLs – the ability to pass a value through a URL. This means we can use it as a common URL base to run the shortcut above for any note just by changing the URL.

Now, honestly, at this point we have the base URL, and you could just manually create the links at this point. For example, “kmtrigger://macro=Open%20Apple%20Note&value=Work%20Ideas” would open my Work Ideas note.

But I don’t do clunky, and typing things out particularly when they involve percent encoding multiple words is one of my least favorite things to do. Thankfully we don’t have to, and for this I give you two options:

Option 1: Keyboard Maestro

I set this up using Keyboard Maestro initially because I’m more familiar with it, and because I already did the legwork, I’m including it here. For those of you who want a universal option, feel free to skip ahead to option 2 which uses Shortcuts instead meaning it will work on Mac OS, iPad OS and iOS.

Using Keyboard Maestro I set up a second macro that works only when I’m in Apple Notes, so that when I press ⌘K it copies the note title I’ve selected and generates the URL for me.

Triggered by any of the following (when Notes is at the front)

This hot key: ⌘K is pressed

Will execute:

Copy Selected Text

Filter System Clipboard with Percent Encode for URL to variable Note Title

Set System Clipboard text to “kmtrigger://macro=Open%20Apple%20Note&value=%Variable%Note Title%”

Now I can generate a link to any Apple Note that can be pasted anywhere on my Mac. If you only ever use a Mac, cool, you’re done, but I suspect most of you are like me and use iPhones and iPads.

Keep reading.

Option 2: Shortcuts

We can do the same thing in Shortcuts using a shortcut that receives text input from the share sheet that percent encodes the selected title, appends it to the base URL, and adds it all back to the clipboard, just like the Keyboard Maestro version, but Shortcuts means unlike the other option, this one will work on Macs, iPhones, and iPads.

Side note: If you want to use it on MacOS, you need to check a box to have this enabled in the services menu and optionally via a keyboard shortcut by going to the Details pane.

One More Thing – Parsing a Keyboard Maestro Link

Now we have our links, but we still need to use them. Again, if we’re just using a Mac with Keyboard Maestro, we’re fine using the links as they are. We’re out of luck if we want to use them on our iPhones or iPads though, which brings us to our last and final piece of the puzzle.

This is simply a shortcut that works in reverse of what we did earlier. Select the URL and select share from the pop up menu. It grabs the selected URL, removes the base Keyboard Maestro URL, percent decodes the URL, and then opens the note with that title.

I’ve only been testing this for a bit, and admittedly my brain is fairly exhausted after putting all this together. I also will never claim to be an expert in Shortcuts or Keyboard Maestro, so there is probably a way more elegant way to do this. I’m open to suggestions. In testing, I’ve only run into a few issues in terms of notes having similar titles or content. In that case, Shortcuts graciously gives you the option to pick the note you want from the results.

Hopefully that helps some of you. I’m off to give my brain a sorely needed break. Happy note taking.

It’s been quite a few months since I’ve posted here. Life just gets in the way sometimes, but have no fear, I’m back, at least for today. In the time since my last post, I’ve gotten rather used to my hybrid work schedule despite initially struggling with it.

To recap, since August, I’ve been alternating working two days (Mondays and Fridays) or three days (Tuesdays-Thursdays) in the office every other week. While the schedule definitely has its benefits, it also has its downsides. The biggest downside is my days spent in the office are far less focused due to various interruptions and distractions throughout the day. To account for this, I looked for ways to add more structure to my weeks and accepted that depending on where I was spending my time, some weeks would just be better suited for certain tasks than others depending on the level of focus they required.

I’ve since begun adding more structure to my days as well, probably because time-blocking (and time-tracking) seems to be a rather popular topic in the circles I find myself in online at the moment.

But… time blocking doesn’t work for me.

As much as my Type A mind really appreciates the detail that comes with planning days out like Cal Newport. I usually end up abandoning my perfectly time-blocked calendar at the first sign of the day deviating from my plan. A part of me even rebels against having a plan for every hour of my day. (Don’t tell that to my other half who’d probably jump for joy at the idea of me not having things planned out in excruciating detail.)

Instead of scheduling out my days, I think of my days as conceptual time blocks starting with morning, afternoon, and evening. This actually harkens back to my Erin Condren Life Planner days which used the exact same blocks of which, surprisingly, I wasn’t a huge fan at the time. From there, I batch my tasks according to how I know I best work, while also adding some variety to make sure I’m not doing one thing for too long.

A typical day might look something like this:

Morning

Administrative Tasks – This block includes things like ordering my tasks in Things 3 making sure things are tagged into their appropriate morning, afternoon, or evening blocks; checking my email; checking my budget in YNAB; and lastly, checking into our ticketing system to triage any support requests that came in overnight.

Personal Administrative Tasks – (Note: If I’m working in the office, I do this first because I need to do these before I get into the office.) This block includes things like getting ready for the day, making the bed, feeding our ancient 18-year-old cat, meditating, and also grabbing a bite to eat.

1st Project/Meeting Block – This is when I work on my 3 tasks for the day. Most of my meetings also tend to be scheduled around this time as well. I get through as much as I can.

Break – Around this time, I start getting restless from sitting. If I’m working from home, I’ll do a quick workout on Apple Fitness Plus. If I’m in the office, I go for a short walk, preferably outside.

Afternoon

Admin Check – I usually circle back to my email and any other communications during this time. Not mentioned above, but I continue monitoring our ticketing system and phone lines constantly throughout the day.

Lunch Break – Self-explanatory, but I also try and fit in some sort of activity in here as well – usually another walk.

2nd Project/Meeting Block – If I haven’t finished my 3 tasks from the morning, I keep working on them here until I finish them. I also get the occasional meeting scheduled around this time.

Evening

Exercise – If I haven’t finished my exercise by this point in the day, this is where I do my scheduled workout (using Apple Fitness Plus).

Evening Chores – I use this time to wrap up any chores I still need to complete for the day. I also use this time to shower, get ready for the next day, meditate, feed the cat, and start dinner.

Evening Shutdown – This is where I look over my to-do list in Things, rescheduling anything I might not have gotten to and scheduling my three tasks for the next day.

Dinner & Free Time – With everything done for the day, I’m free to finally sit down on the couch with something to eat and relax however I please.

The beauty of this structure is it’s easy to start each morning with a general idea of how I’m going to approach my to-do list without scheduling tasks or my calendar being so rigid that any slight deviation throws my day out of wack. It also takes into account how I best work – giving me time during the mornings to work on things that require the most focus, allowing for movement and mental breaks throughout the day, and also allowing for buffer time if things take longer or come up throughout the day.

I’m not sure if this is helpful to anyone, but if it has been or you have any questions, feel free to reach out.

We’ve been using Apple’s Reminders app as our shared grocery list for years now. We use it for two main reasons:

It can be shared between myself and my significant other. This means we can both add things to it throughout the week, and we both have access to the list depending on who actually does the shopping.

It syncs with our recipe manager, Paprika.

As Reminders has evolved to include new features, so to has how we use it for our shopping list.

Adding a Link to the Store Ad

At the top of our list, I keep a standing reminder that just includes a link to the weekly store ad for the grocery store we normally shop at, Aldi. This makes it easy to check what’s on sale when I’m making the list.

Using Subtasks to Categorize by Aisle

I’d say the biggest change to how we use our shopping list came with iOS 13’s introduction of subtasks. Because we generally shop at the same store, we have headings for each section of the store (in all caps so they stand out), organized in the order of the store. Actual grocery items are then listed as subtasks. This means that as long as we’re paying attention, we can go through the store in one direction without having to double back for an ingredient.

Using Show Completed When Making the List

When putting together the grocery list, I toggle show completed. This gives me a running list of things we’ve added in the past, making it an easy trigger list to see staples I might have missed. If I see something we need, I’ll uncheck it.

Worth noting here, I tend to add things throughout the week as we run out, so occasionally I end up with two copies of those staples (the completed one, and the incomplete one I added through Siri). In these cases, I delete the duplicate to keep the “Show Completed” from becoming a cluttered mess.

Location-Based Reminders

I mentioned earlier that we primarily shop at Aldi. However, Aldi doesn’t always have everything we need, or we just prefer to buy certain things at other stores. In these cases, I have an “Other” section at the bottom of our list and list those special buys as subtasks. For each subtask I set a location-based reminder so that when we’re near that particular store, say Costco, I get a notification that we need something.

I’m curious, do you use Reminders or another app for your grocery list? Do you just throw things on it like I used to do? Do you have one big list or lists by store? Let me know in the comments.

In a recent blog post, I wrote about how I’ve been looking for ways to add more structure to my weeks after finding that switching back and forth between working from home and working in the office was throwing my productivity out of wack.

I’ve spent the last month or so soaking in all the advice I could find online in terms of weekly planning. Special thanks goes out to Peter Akkies and michelleb who I found particularly inspiring during my search.

I’d also like to give a shoutout to the Cultured Code team. I didn’t know it at the time, but what they had in the works for their iPadOS 15 update turned out to be a huge help as well.

So what’s changed with how I’m planning out my tasks?

First things first, let’s talk about what Cultured Code added to Things 3 in their iOS 15 update – namely the extra large “Up Next” widget. This widget shows your to-dos for Today, Tomorrow, and the two days after that. This was actually something I had tried to create on my own in just about every productivity tool (TeuxDeux, Trello, AirTable, Notion, etc) but abandoned because it felt like I was wasting time duplicating content that was already in Things 3. Now that it’s built into Things 3, problem solved.

I’d honestly prefer to see a full week (XXL widgets in iOS 16 maybe?), but three days has worked just fine. Seeing my tasks in listed out for the next few days horizontally makes it easy to see days when I’m overcommitted or, on the rare occasion, not committed enough so that I can go into Things 3 and reschedule some things.

Seeing what’s on my plate this way has led to some other changes in how I approach my planning as well.

I no longer try to schedule additional tasks more than one day ahead. I found that scheduling tasks out for the entire week rarely worked for me. I’m much more likely to accomplish what I set out to do if I plan the night before.

When I am planning out my day the night before, I try not to schedule more than 3 additional (not scheduled/routine) tasks from Anytime for the next day. Three feels like the right number in terms of feeling like I’m making progress without feeling like I’m waking up to a daunting to do list.

I also have a repeating project called “Priorities for the Week” that I use to set three priorities for the upcoming week during my weekly reviews. The priorities I list in this project are tasks that link to other projects or tasks in Things. For instance, one of my priorities for this week, is to finish this blog post, so I have that listed in my priorities project, and the task itself links to the corresponding “Post to Blog” project to make it easy to check off both I do post this blog post, and the priorities project itself is set to start every week on Monday where it then stays in my Today view until I check everything off.

I’ve nested this project within a new area, Goals, which lives at the very top of my areas list so that Priorities for the Week shows up at the top of Today. The goals area also has a project for this year’s goals so I can clearly keep track of them, and I’ve already started on planning 2022’s goals in their own project as well.

Having been using these methods for the past several weeks, I can confidently say they have helped me feel like I’m actually making progress on my goals rather than responding to whatever comes my way.

A side effect of this setting is that I could no longer manually order my tasks to reflect the order I planned to do them during the day. As I shared in that earlier post, when first made the switch, I thought I’d be fine with this tradeoff because my areas and their respective projects are ordered by priority. This meant my highest priority tasks were always at the top for me to do first thing in the morning.

In theory, this change was great for my workflow. In practice, it was less so.

Sometimes those highest priority tasks weren’t things I could do in the morning. Making a handful of phone calls while the other half is still sound asleep in the next room probably wouldn’t go over well. Similarly, if my morning was full of appointments, I probably wouldn’t have time to handle putting together a report. I also tend to work better on reports in the afternoon anyway.

At the time of making that change, I even noted that I was already finding myself jumping around in the list. Little did I know just how much jumping I would end up doing. Over time, I found myself spending a LOT of mental bandwidth simply scanning through my list multiple times a day to figure out what I could work on next.

Ordering my list manually allowed me to build out a plan for my day every morning, and I no longer had that plan.

My solution ended up being a fairly straightforward method that I adopted from my Erin Condren paper planner days. While there’s now a few different layouts, the original Erin Condren planners I used broke each day down into three blocks, Morning, Afternoon, and Evening.

Things 3 already has a This Evening section, but I’ve manually created tags for This Morning and This Afternoon. (Cultured Code, if you’re listening, an option to have a This Morning or This Afternoon section could be nice.)

On mornings where I’m feeling a little more overwhelmed, I can go through and find all the tasks in my Today view that I need and can do first thing in the morning and tag them with my morning tag and (optionally) do the same with the afternoon tag.

Once I’m done, I can filter my Today list by the This Morning tag which reduces my Today list to only tasks I can do that morning and nothing more.

I’ve been using this method for a few weeks and I’m actually really liking it.

It’s also a bit reminiscent of my days using Omnifocus’s start times which prevented things from showing up until I could truly do them. As an Omnifocus user, I loved start times. Why see a task before you can work on it?

I’ll tell you why.

I’d start my day with no clue of how many tasks were scheduled. I’d check everything off for the day and revel in the feeling that my tasks were done, not knowing another task (or tasks) had a start time later in the day.

In the worst case scenario, I wouldn’t see those tasks until the next day missing them entirely. The more common scenario was that my task list started to seem neverending – “Congratulations! You’ve done all your tasks for the day! Just kidding! Here’s another one at 9PM!”

The lack of start times in Things 3 was actually a good thing for my life, but I still did miss that ability to filter things.

Now by using tags in Things 3, I still see every task I have on my Today list at the start of the day so I know what I’m in for, but I also have the option of breaking it down further if necessary.

This last month marked my one year anniversary of using the app, You Need a Budget, or YNAB, and to say I’ve been dying to share my progress is an understatement.

I figured YNAB would be one of those things to pass the time while stuck at home during the pandemic. At the very least it’d be something to do during the couple weeks I’d be stuck at home. Little did I know, I’d still be here a year later, and little did I know much YNAB would change my finances during that time.

I want to start out by saying I’ve been incredibly lucky to not only keep my job during this past year, but also by being able to work from home this whole time. I truly feel for those who didn’t share my situation.

Regardless of what my situation had been, finding YNAB at the start of the pandemic couldn’t have been better timing. The world was facing the uncertainty of a pandemic, and I was almost $9000 in debt with basically nothing in the bank.

Creating a Plan

My first month of using YNAB was all about creating a plan. It turns out despite using Mint for all these years, I really had no clue what to do with my money. If there was more than $1000 in the bank, I figured it was safe to spend, so I did. Instead, I had a great idea of where my money went in the form of nagging “overspending” alerts, which weren’t all that helpful after I’d spent my money. YNAB flipped Mint’s budgeting model on its head and forced me to create a plan for every dollar (rule 1) before I spent it.

Paying Off Credit Cards

My second month of using YNAB ended up being one of those rare months full of unexpected money (why can’t they all be like that!) – a 3 paycheck month, tax refunds, and a stimulus check. In the past, I would have squandered this extra money on random things from Amazon, but armed with my plan, I put the extra money to work for me towards the goals I had set out.

My first goal was to pay off my credit cards, which I’d been unsuccessful at doing pretty much ever since I got the cards. Thankfully, I never wracked up tons of credit debt, but I always seemed to have some combination of around $2000-4000.

Thanks to the extra income in April, I was able to pay off all three of my credit cards. My initial goal was to pay off 1 card by the end of 2020. I’m also happy to say that thanks to the way YNAB forces you to treat credit cards as if they’re debit cards, I’ve continued to completely pay off my cards each month ever since. Getting paid to use a credit card is a lot better than paying interest.

Paying Off the Car

My second goal was paying off my car. Pre-YNAB this seemed like a goal I’d be able to tackle by December 2021 at the earliest, but I ended up doing it in August of 2020. This was actually an even bigger deal to me because I actually accomplished another goal, of becoming debt-free other than the mortgage by the time I celebrated my 30th birthday which I hadn’t even imagined being possible 2 months prior.

Feeling YNAB Broke

One of the reasons I was consistently over budget using Mint was that I wasn’t planning for what YNAB considers True Expenses (rule 2) – things like that yearly Amazon Prime subscription, a new set of tires, or the appliance that inevitably gives out at the worst time. Every month one or more of these true expenses would pop up, and because I hadn’t planned for them, I’d pull out the credit card to pay for them.

With YNAB, I started setting aside money for those true expenses. As each one came up, I added it to my budget and started saving a little for it each month. Eventually I was able to convert a number of my monthly bills to annual plans saving even more money.

As a result, my bank balances started to climb, which is also around the time I started feeling “YNAB Broke” as YNABers like to say. My bank account had more money in it than I’d ever had, but suddenly all those dollars already had jobs. I didn’t have $10,000 in the bank to spend on whatever I wanted. It was already earmarked for car insurance or Christmas gifts.

As time went on, I stopped noticing my bank balances altogether. Category balances are what I check, and since they rarely have more than a few hundred dollars in them, you feel broke even though you have more money.

Getting a Month Ahead

One of YNAB’s other tenants is to try and break the paycheck to paycheck cycle by getting a month ahead (or in other words, using last month’s income to pay this month’s bills). It’s rule 4 and they call it aging your money.

This was one of those things that seemed a bit overblown to me but turned out to be unexpectedly rewarding. Each month as my debts went down and more of my true expenses were accounted for, paychecks seemed to get me funded a little further down the budget until one day I realized the whole month was funded and I was still expecting another paycheck for the month. It seems simple, but starting the month knowing everything is accounted for has added so much peace of mind to my life.

Building My Emergency Fund

After getting a month ahead, I refocused my sights on my emergency fund. I had saved up $1000 (Dave Ramsey’s Baby Step 1), but my eventual goal is to have 6 months worth of expenses. I currently have around 2 months of expenses saved for this. Paired with being a month ahead and saving for true expenses, I consider this really a 3 month emergency fund, which brings us to today.

My Goals for 2021

Finally feeling secure in my finances for the first time in my life, I pushed pause on increasing my 3 month emergency fund to 6, and set my sights on the future.

I recently opened a Roth IRA with M1 Finance, and pressed paused on the emergency fund because I wanted to max out my Roth IRA for 2020 and knew I only had until April to do this. (The IRS has since extended the deadline to May.) As of this past March, I’ve reached my goal. Going forward, I’ve built monthly contributions of $500 into my budget so that so I won’t need to play catch up to max out my contributions for years going forward.

My other goals for the rest of the year, all of which I’m on track to complete, are as follows:

Finish saving for our wedding

Refinance our condo to a 15 year mortgage

Complete saving a full 6 months worth of expenses in case of an emergency

Looking Back

Prior to finding YNAB, I assumed I just didn’t make enough money and my financial situation doomed unless I got another job. I felt stuck with no way up. It turns out my income wasn’t the problem. It was my behavior.

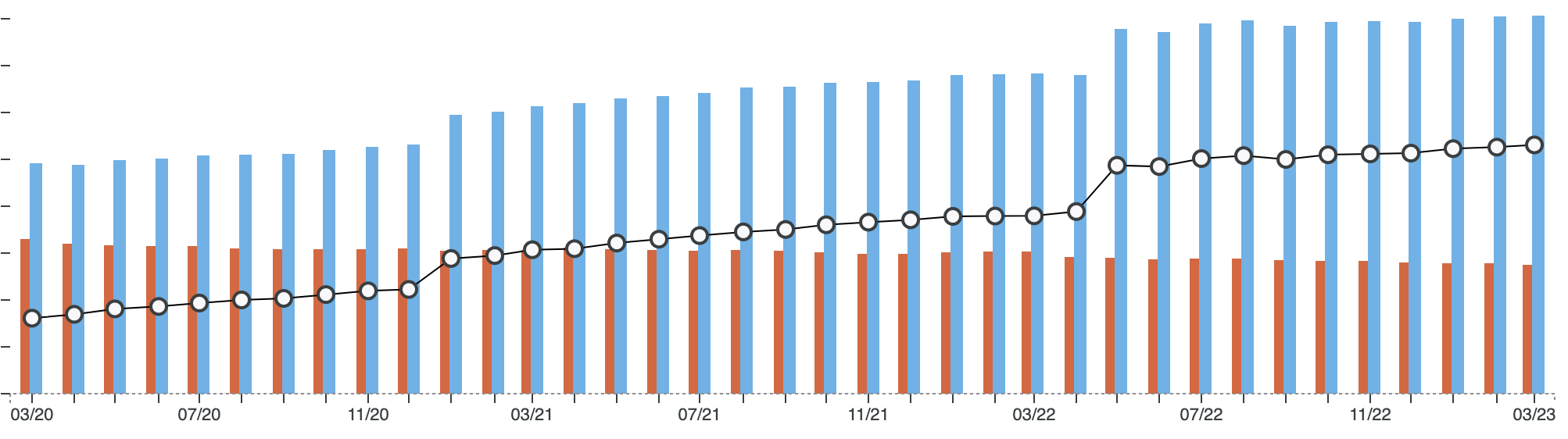

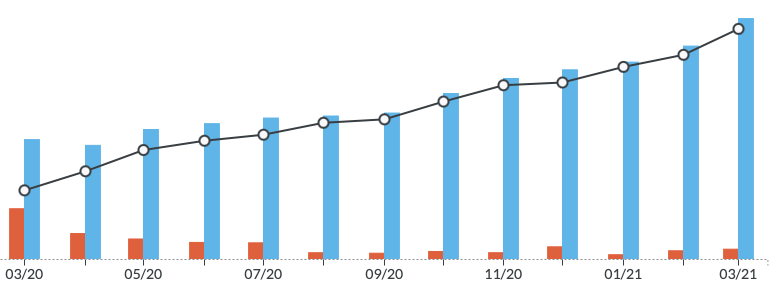

In just one year, I went from living paycheck to paycheck and $9000 in debt to being debt free. The net worth graph from the past year says it all.

(Note: I’ve excluded my mortgage and retirement in the above graph because they really skew the graph making progress hard to see, but with all my accounts included, my net worth has gone up a total of 90.6%. Also worth noting the red debt you see after 8/20 are just my credit cards, which I pay in full each month, carrying over between months.)

My friends and family think I’m a bit YNAB-obsessed, and truthfully I am constantly singing its praises. I’ve definitely drank the Kool-aid, but honestly, if you’d shown me this graph a year ago and told me it would be mine today, I wouldn’t have believed you. Trying YNAB has truly been one of the best decisions I’ve made and if this is the progress I made in one year, I can’t wait to see what’s in store for the future.

And if you want to try YNAB for yourself, the links to it included on this page will get us both an extra free month if you choose to sign up after the 34 day free trial. Did I mention there’s no credit card required to sign up, so it’s totally risk free. They aren’t some sketchy company that will immediately sign you up at the end of the trial.

The reason for my dabbling was due to a feeling of uneasiness when using Evernote. For years, I’ve been increasingly less and less confident in the Evernote’s future or the company’s values, but in the absence of no better alternative, I stuck around hoping the tides would turn.

Suffice to say, the tides haven’t turned, and their recent app updates removed several of my most used features. Sure, Evernote keeps saying that they’ll bring these features back in the future, but this is also the same Evernote who said the new versions would be better than ever. Spoiler alert: They’re not.

One thing that has changed, however, is the world of Evernote competitors. It’s hard to say there are no better alternatives anymore, especially now that my needs have simplified, which is why I started thinking about what I truly needed out of a personal knowledge management system.

Topping the list of must-need features:

I need to be able to save important emails easily for reference.

I need to be able to add multiple file types.

I need to be able to link to notes both within and outside of the system.

My obvious first choice would have been Apple Notes, which I’m already using for sharing notes with my other half. Unfortunately, while it does meet most of my needs, it doesn’t have any sort of integration with my email app. Note links are also quite clunky. You pretty much have to pretend to share the note with someone to get a note link.

The highly-praised Notion was next on my list, but quite honestly I don’t have the patience to set up a database from scratch.

I also tried OneNote, but, my gosh, the interface is “oh-so-Microsoft Office” and seemed way too fiddly for my needs. No thank you.

At this point, I’ve settled with Bear. I’m still getting used to the tag-based structure, but overall, I’ve been liking it a lot more than I expected. This is in part to the simplification of my organizational needs from when I last tried it. There are a few things I do miss, like tables, but those seem to be on the road map so hopefully, the wait won’t be too terribly long. It’s also worth mentioning that Bear’s Pro subscription is around 20% of what a year of Evernote Premium would cost me.

With that said, I really do hope the best for Evernote. As a note-taking service, it’s still a pretty great option for most users, I’m just not sure I’m most users anymore. If they can prove me wrong, I’m still keeping my options open, but for now Bear seems to be my best bet.