We’ve been using Apple’s Reminders app as our shared grocery list for years now. We use it for two main reasons:

It can be shared between myself and my significant other. This means we can both add things to it throughout the week, and we both have access to the list depending on who actually does the shopping.

It syncs with our recipe manager, Paprika.

As Reminders has evolved to include new features, so to has how we use it for our shopping list.

Adding a Link to the Store Ad

At the top of our list, I keep a standing reminder that just includes a link to the weekly store ad for the grocery store we normally shop at, Aldi. This makes it easy to check what’s on sale when I’m making the list.

Using Subtasks to Categorize by Aisle

I’d say the biggest change to how we use our shopping list came with iOS 13’s introduction of subtasks. Because we generally shop at the same store, we have headings for each section of the store (in all caps so they stand out), organized in the order of the store. Actual grocery items are then listed as subtasks. This means that as long as we’re paying attention, we can go through the store in one direction without having to double back for an ingredient.

Using Show Completed When Making the List

When putting together the grocery list, I toggle show completed. This gives me a running list of things we’ve added in the past, making it an easy trigger list to see staples I might have missed. If I see something we need, I’ll uncheck it.

Worth noting here, I tend to add things throughout the week as we run out, so occasionally I end up with two copies of those staples (the completed one, and the incomplete one I added through Siri). In these cases, I delete the duplicate to keep the “Show Completed” from becoming a cluttered mess.

Location-Based Reminders

I mentioned earlier that we primarily shop at Aldi. However, Aldi doesn’t always have everything we need, or we just prefer to buy certain things at other stores. In these cases, I have an “Other” section at the bottom of our list and list those special buys as subtasks. For each subtask I set a location-based reminder so that when we’re near that particular store, say Costco, I get a notification that we need something.

I’m curious, do you use Reminders or another app for your grocery list? Do you just throw things on it like I used to do? Do you have one big list or lists by store? Let me know in the comments.

In a recent blog post, I wrote about how I’ve been looking for ways to add more structure to my weeks after finding that switching back and forth between working from home and working in the office was throwing my productivity out of wack.

I’ve spent the last month or so soaking in all the advice I could find online in terms of weekly planning. Special thanks goes out to Peter Akkies and michelleb who I found particularly inspiring during my search.

I’d also like to give a shoutout to the Cultured Code team. I didn’t know it at the time, but what they had in the works for their iPadOS 15 update turned out to be a huge help as well.

So what’s changed with how I’m planning out my tasks?

First things first, let’s talk about what Cultured Code added to Things 3 in their iOS 15 update – namely the extra large “Up Next” widget. This widget shows your to-dos for Today, Tomorrow, and the two days after that. This was actually something I had tried to create on my own in just about every productivity tool (TeuxDeux, Trello, AirTable, Notion, etc) but abandoned because it felt like I was wasting time duplicating content that was already in Things 3. Now that it’s built into Things 3, problem solved.

I’d honestly prefer to see a full week (XXL widgets in iOS 16 maybe?), but three days has worked just fine. Seeing my tasks in listed out for the next few days horizontally makes it easy to see days when I’m overcommitted or, on the rare occasion, not committed enough so that I can go into Things 3 and reschedule some things.

Seeing what’s on my plate this way has led to some other changes in how I approach my planning as well.

I no longer try to schedule additional tasks more than one day ahead. I found that scheduling tasks out for the entire week rarely worked for me. I’m much more likely to accomplish what I set out to do if I plan the night before.

When I am planning out my day the night before, I try not to schedule more than 3 additional (not scheduled/routine) tasks from Anytime for the next day. Three feels like the right number in terms of feeling like I’m making progress without feeling like I’m waking up to a daunting to do list.

I also have a repeating project called “Priorities for the Week” that I use to set three priorities for the upcoming week during my weekly reviews. The priorities I list in this project are tasks that link to other projects or tasks in Things. For instance, one of my priorities for this week, is to finish this blog post, so I have that listed in my priorities project, and the task itself links to the corresponding “Post to Blog” project to make it easy to check off both I do post this blog post, and the priorities project itself is set to start every week on Monday where it then stays in my Today view until I check everything off.

I’ve nested this project within a new area, Goals, which lives at the very top of my areas list so that Priorities for the Week shows up at the top of Today. The goals area also has a project for this year’s goals so I can clearly keep track of them, and I’ve already started on planning 2022’s goals in their own project as well.

Having been using these methods for the past several weeks, I can confidently say they have helped me feel like I’m actually making progress on my goals rather than responding to whatever comes my way.

I used to be the first in line excited to buy new technology, particularly Apple products – So much so, that friends and family dubbed me iAndrea. I won’t lie, I looked like a pop-up Apple Store at times having all my devices spread out in front of me, but those times have passed. I’m still happily using my iPhone XS and my Apple Watch 4, and my iPad, and computer are definitely showing their age at 5 years old. The products being released these days, from Apple and other companies, just haven’t been compelling enough for me to purchase.

That is until yesterday.

Yesterday Amazon announced an all new Kindle Paperwhite, and to say it checked all the boxes of what I was hoping for is an understatement.

I’ve been faithfully using my Kindle Paperwhite from 2013 all these years and it’s served me well enough that I never needed to upgrade.

It’s even served this blog well over the years as my post on adding wireless charging to it has been one of the top ranking posts of all time. For a while it was even the top search result when you searched for wireless charging Kindle.

I couldn’t be more excited to upgrade my Kindle to this device after all these years. I even moved money around in my budget to move up my “New Kindle” purchase sooner.

If you’re not interested in wireless charging, you can save yourself $50 and get the standard model which is still pretty fantastic, but I’ve gone full in on the wireless charging lifestyle so it’s worth the convenience.

In addition to wireless charging (on the Signature Edition), both new Paperwhite models also switch to USB-C for charging and include a larger screen with an adjustable warm light. The Signature Edition also features auto-adjusting light sensors.

Coming from an ancient model, I’ll also be able to take advantage of the flush screen, waterproof rating, and bluetooth audio.

I couldn’t be more pleased with the new Kindle, and although I’m sad I’ll likely be losing some of my blog revenue due to people no longer needing wireless charging adapters, I think this Kindle is going to be a great device for so many people.

Do you use a Kindle or other e-reader? What are your thoughts on them or the new Kindle Paperwhite?

*Amazon didn’t ask me to write this, although there are affiliate links in this post. I truly just adore my Kindle and haven’t been this excited for a new product in a while.

People have been talking about getting back to normal (or at least a new normal) post-pandemic for months now.

For the past few months I wasn’t quite sure what that would look like for me. While my particular office functioned well remotely, the university I worked at understandably wants folks back in the office for the students that are on campus.

The months leading up to this past week (the first week of classes) felt like I was in limbo. Somehow I was faced with planning a socially distant office space having never done so all while dealing with the reality that my time working from home was about to come to an abrupt end. Queue anxiety.

Thankfully for now, I’ve been able to continue teleworking 2-3 days a week, but it’s far from the telework environment I’ve gotten used to.

My team is now split pretty much 90% remote and 10% on site. For the staff working on campus, we’re faced with a new challenge of managing our usual workload plus, often times, singlehandedly managing the workload of customers who walk in with questions, most of which isn’t even related to our job but rather to the building we’re in. Pre-pandemic, that walk-in support would have been split among 3-5 people instead of 1-2.

Did I mention we’re also navigating this through our busiest time of the year where our work quadruples anyway?

While I’m thankful to be able to not be fully back in the office, it’s safe to say that I feel as though my routine is now thoroughly upended. Because my teleworking schedule changes every other week, I now understand my partner’s tendency to never know what day of the week it is. I also can’t seem to get into a normal rhythm of work. All in all, I just feel disheveled.

So what’s next?

I find myself wanting to make a weekly plan, but the day to day unpredictability of tech support has proved that to be challenging.

I’ve also found myself revisiting the maker/manager schedule. My current telework schedule is structured such that the weeks I am in the office 3 days a week also tend to be my meeting heavy weeks, so I’m toying with the idea of a accepting that those weeks will simply be distraction heavy and using my three telework days the following week to really focus on projects.

Anyway, this is a bit of a rambling post, but I wanted to throw my two cents out there in case anyone else is struggling or has struggled with something similar.

A side effect of this setting is that I could no longer manually order my tasks to reflect the order I planned to do them during the day. As I shared in that earlier post, when first made the switch, I thought I’d be fine with this tradeoff because my areas and their respective projects are ordered by priority. This meant my highest priority tasks were always at the top for me to do first thing in the morning.

In theory, this change was great for my workflow. In practice, it was less so.

Sometimes those highest priority tasks weren’t things I could do in the morning. Making a handful of phone calls while the other half is still sound asleep in the next room probably wouldn’t go over well. Similarly, if my morning was full of appointments, I probably wouldn’t have time to handle putting together a report. I also tend to work better on reports in the afternoon anyway.

At the time of making that change, I even noted that I was already finding myself jumping around in the list. Little did I know just how much jumping I would end up doing. Over time, I found myself spending a LOT of mental bandwidth simply scanning through my list multiple times a day to figure out what I could work on next.

Ordering my list manually allowed me to build out a plan for my day every morning, and I no longer had that plan.

My solution ended up being a fairly straightforward method that I adopted from my Erin Condren paper planner days. While there’s now a few different layouts, the original Erin Condren planners I used broke each day down into three blocks, Morning, Afternoon, and Evening.

Things 3 already has a This Evening section, but I’ve manually created tags for This Morning and This Afternoon. (Cultured Code, if you’re listening, an option to have a This Morning or This Afternoon section could be nice.)

On mornings where I’m feeling a little more overwhelmed, I can go through and find all the tasks in my Today view that I need and can do first thing in the morning and tag them with my morning tag and (optionally) do the same with the afternoon tag.

Once I’m done, I can filter my Today list by the This Morning tag which reduces my Today list to only tasks I can do that morning and nothing more.

I’ve been using this method for a few weeks and I’m actually really liking it.

It’s also a bit reminiscent of my days using Omnifocus’s start times which prevented things from showing up until I could truly do them. As an Omnifocus user, I loved start times. Why see a task before you can work on it?

I’ll tell you why.

I’d start my day with no clue of how many tasks were scheduled. I’d check everything off for the day and revel in the feeling that my tasks were done, not knowing another task (or tasks) had a start time later in the day.

In the worst case scenario, I wouldn’t see those tasks until the next day missing them entirely. The more common scenario was that my task list started to seem neverending – “Congratulations! You’ve done all your tasks for the day! Just kidding! Here’s another one at 9PM!”

The lack of start times in Things 3 was actually a good thing for my life, but I still did miss that ability to filter things.

Now by using tags in Things 3, I still see every task I have on my Today list at the start of the day so I know what I’m in for, but I also have the option of breaking it down further if necessary.

First of all, wow it’s been a long time. Sorry for not posting since May. I feel like I blinked and now we’re already more than halfway through 2021. Full disclosure though, I also haven’t had a lot of inspiration to write either. Posts that seem to do well on here are typically related to Things 3 or note taking, and quite frankly, my system doesn’t really change all that much to have new things to write about.

When I found Getting Things Done (GTD) in high school, it was life changing. The methodology just clicked and I never looked back. Whether I was using Things 2, a Filofax, Omnifocus, or now, Things 3, GTD has always been the backbone of how I manage life.

My concept of GTD has changed significantly over the years. GTD is one of the few books I reread every few years. Each time I read it the book seems to hit differently and I grasp the concepts a little more. Every so often I also find myself having small breakthroughs where a concept clicks just a little more. While the breakthroughs seem to be fewer and far between these days, I do have occasional moments where I still find my GTD practice changing.

In the past, examples have included fully understanding what capturing everything actually entails (It’s more than you think!), why something that takes more than one step really should be a project and not a single action, and why it actually can be sufficient to only have a single next action in a project rather than planning every detail out at the start.

My most recent breakthrough is understanding mind like water.

For much of the past year and a half, I’ve run myself ragged, stressing about all the projects I was responsible for, many of which I had never encountered like managing a remote team, setting up a socially distanced office, planning a return to the office when the conditions seem to be shifting daily (go get vaccinated folks!), or dealing with a sick pet.

In every one of these cases, most of the stress was due to simply not knowing what to do next, and as more and more of these piled up, the overwhelm set in hard.

In a recent chat with my therapist, we discussed how one of my coping mechanisms for stress is creating systems and solving problems. Sadly I usually do this out of desperation rather than regular practice. Rather than feeling helpless in a situation, her suggestion was to shift my thinking and problem solve at least one thing I could do to make me feel more at ease – to make a stressful situation a little less scary.

In writing this, I find myself realizing this probably sounds a lot like next actions, but I actually think about it a little differently.

For next actions, I ask myself the question, “What is the next thing that needs to get done to move this project forward?” This question is all about progress and completion.

For mind like water, I’m asking myself, “What is something I could do to feel more at ease?” Here I’m more concerned about what’s going to make me feel better.

In some cases, the answers to these questions might even be the same. In my sick pet example, the next action was to clearly call the vet to schedule an appointment. However, I found myself stalling because I hate making phone calls, how busy my vet is, how much my pet hates going to the vet, and how scary the diagnosis could be. All of these things were overwhelming, but what was more overwhelming? Knowing my pet was sick, not knowing why, constantly telling myself I should be calling to schedule an appointment, and beating myself up for not doing it because I’m a responsible pet owner. Without question, the thing to put me more at ease was to just make the call.

It’s a small mindset shift, but in cases where I’m truly feeling stressed, it’s that small shift that takes me from feeling like things are out of control and helpless to seeing a path through.

One of the things I’ve struggled with for most of my life is maintaining a sustainable pace. I’m someone who tends to run non-stop until I’m overwhelmed and exhausted leaving me with barely enough energy to get out of bed.

Over the past few months, I’ve been coming to terms with how sustainable that lifestyle actually is (It’s not!) which has lead me to build intentional pauses into my life rather than being forced to take them.

By taking these pauses, I’ve learned a few things about myself:

Things that should be relaxing aren’t anymore. For instance, playing Animal Crossing has become just another thing to check off my to-do list each day.

Taking a break seems like I luxury I can’t afford. I often find myself making excuses for why I shouldn’t take even 60-second break because I should be doing other things. Never mind, how much time I spend on Reddit though…

My ability to focus has become nonexistent. Whether I’m pausing for 5 minutes or 60 seconds, the struggle is real keeping my brain from jumping to the next task.

Sadly, as I’ve mentioned this way of life just isn’t sustainable. Constantly rushing from one thing to the next means I’m in a state of constant stress and anxiety, which can and has lead to real health consequences.

Knowing my strengths lie in finding solutions and staying on schedule, I’ve started scheduling 2 short meditations (5 minutes usually) every day – once in the morning and once in the afternoon. Like exercise, I now consider these non-negotiable.

Some days I use a guided meditation. My current and free app of choice is Insight Timer. Other days I use the Breathe function on my watch. Other days I just honestly use the time to do nothing.

The important part isn’t how well I do or what I do. It’s actually teaching my body a new baseline of reactivity. Honestly, it seems silly to think that I’m having to teach my body to relax, but, then again, after all that’s happened in the past 12 months or so, nothing about this world surprises me.

This last month marked my one year anniversary of using the app, You Need a Budget, or YNAB, and to say I’ve been dying to share my progress is an understatement.

I figured YNAB would be one of those things to pass the time while stuck at home during the pandemic. At the very least it’d be something to do during the couple weeks I’d be stuck at home. Little did I know, I’d still be here a year later, and little did I know much YNAB would change my finances during that time.

I want to start out by saying I’ve been incredibly lucky to not only keep my job during this past year, but also by being able to work from home this whole time. I truly feel for those who didn’t share my situation.

Regardless of what my situation had been, finding YNAB at the start of the pandemic couldn’t have been better timing. The world was facing the uncertainty of a pandemic, and I was almost $9000 in debt with basically nothing in the bank.

Creating a Plan

My first month of using YNAB was all about creating a plan. It turns out despite using Mint for all these years, I really had no clue what to do with my money. If there was more than $1000 in the bank, I figured it was safe to spend, so I did. Instead, I had a great idea of where my money went in the form of nagging “overspending” alerts, which weren’t all that helpful after I’d spent my money. YNAB flipped Mint’s budgeting model on its head and forced me to create a plan for every dollar (rule 1) before I spent it.

Paying Off Credit Cards

My second month of using YNAB ended up being one of those rare months full of unexpected money (why can’t they all be like that!) – a 3 paycheck month, tax refunds, and a stimulus check. In the past, I would have squandered this extra money on random things from Amazon, but armed with my plan, I put the extra money to work for me towards the goals I had set out.

My first goal was to pay off my credit cards, which I’d been unsuccessful at doing pretty much ever since I got the cards. Thankfully, I never wracked up tons of credit debt, but I always seemed to have some combination of around $2000-4000.

Thanks to the extra income in April, I was able to pay off all three of my credit cards. My initial goal was to pay off 1 card by the end of 2020. I’m also happy to say that thanks to the way YNAB forces you to treat credit cards as if they’re debit cards, I’ve continued to completely pay off my cards each month ever since. Getting paid to use a credit card is a lot better than paying interest.

Paying Off the Car

My second goal was paying off my car. Pre-YNAB this seemed like a goal I’d be able to tackle by December 2021 at the earliest, but I ended up doing it in August of 2020. This was actually an even bigger deal to me because I actually accomplished another goal, of becoming debt-free other than the mortgage by the time I celebrated my 30th birthday which I hadn’t even imagined being possible 2 months prior.

Feeling YNAB Broke

One of the reasons I was consistently over budget using Mint was that I wasn’t planning for what YNAB considers True Expenses (rule 2) – things like that yearly Amazon Prime subscription, a new set of tires, or the appliance that inevitably gives out at the worst time. Every month one or more of these true expenses would pop up, and because I hadn’t planned for them, I’d pull out the credit card to pay for them.

With YNAB, I started setting aside money for those true expenses. As each one came up, I added it to my budget and started saving a little for it each month. Eventually I was able to convert a number of my monthly bills to annual plans saving even more money.

As a result, my bank balances started to climb, which is also around the time I started feeling “YNAB Broke” as YNABers like to say. My bank account had more money in it than I’d ever had, but suddenly all those dollars already had jobs. I didn’t have $10,000 in the bank to spend on whatever I wanted. It was already earmarked for car insurance or Christmas gifts.

As time went on, I stopped noticing my bank balances altogether. Category balances are what I check, and since they rarely have more than a few hundred dollars in them, you feel broke even though you have more money.

Getting a Month Ahead

One of YNAB’s other tenants is to try and break the paycheck to paycheck cycle by getting a month ahead (or in other words, using last month’s income to pay this month’s bills). It’s rule 4 and they call it aging your money.

This was one of those things that seemed a bit overblown to me but turned out to be unexpectedly rewarding. Each month as my debts went down and more of my true expenses were accounted for, paychecks seemed to get me funded a little further down the budget until one day I realized the whole month was funded and I was still expecting another paycheck for the month. It seems simple, but starting the month knowing everything is accounted for has added so much peace of mind to my life.

Building My Emergency Fund

After getting a month ahead, I refocused my sights on my emergency fund. I had saved up $1000 (Dave Ramsey’s Baby Step 1), but my eventual goal is to have 6 months worth of expenses. I currently have around 2 months of expenses saved for this. Paired with being a month ahead and saving for true expenses, I consider this really a 3 month emergency fund, which brings us to today.

My Goals for 2021

Finally feeling secure in my finances for the first time in my life, I pushed pause on increasing my 3 month emergency fund to 6, and set my sights on the future.

I recently opened a Roth IRA with M1 Finance, and pressed paused on the emergency fund because I wanted to max out my Roth IRA for 2020 and knew I only had until April to do this. (The IRS has since extended the deadline to May.) As of this past March, I’ve reached my goal. Going forward, I’ve built monthly contributions of $500 into my budget so that so I won’t need to play catch up to max out my contributions for years going forward.

My other goals for the rest of the year, all of which I’m on track to complete, are as follows:

Finish saving for our wedding

Refinance our condo to a 15 year mortgage

Complete saving a full 6 months worth of expenses in case of an emergency

Looking Back

Prior to finding YNAB, I assumed I just didn’t make enough money and my financial situation doomed unless I got another job. I felt stuck with no way up. It turns out my income wasn’t the problem. It was my behavior.

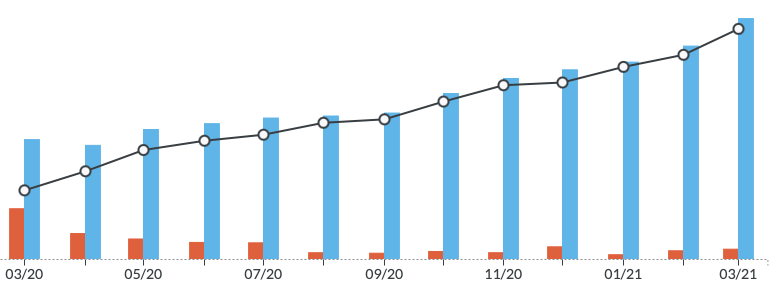

In just one year, I went from living paycheck to paycheck and $9000 in debt to being debt free. The net worth graph from the past year says it all.

(Note: I’ve excluded my mortgage and retirement in the above graph because they really skew the graph making progress hard to see, but with all my accounts included, my net worth has gone up a total of 90.6%. Also worth noting the red debt you see after 8/20 are just my credit cards, which I pay in full each month, carrying over between months.)

My friends and family think I’m a bit YNAB-obsessed, and truthfully I am constantly singing its praises. I’ve definitely drank the Kool-aid, but honestly, if you’d shown me this graph a year ago and told me it would be mine today, I wouldn’t have believed you. Trying YNAB has truly been one of the best decisions I’ve made and if this is the progress I made in one year, I can’t wait to see what’s in store for the future.

And if you want to try YNAB for yourself, the links to it included on this page will get us both an extra free month if you choose to sign up after the 34 day free trial. Did I mention there’s no credit card required to sign up, so it’s totally risk free. They aren’t some sketchy company that will immediately sign you up at the end of the trial.

As many of you might have noticed, I ended up taking a much longer break from the blog than anticipated last year, but I didn’t want to miss out on posting my yearly recap and focus for the new year.

In all honesty though, my year of health turned out to be a success. By implementing little changes consistently, I was able to increase my daily activity from around 6 minutes of exercise to 28 minutes. Technically, I’m on a streak of closing all of my activity rings including 30 minutes of exercise for 51 days straight though, and for once, I’d consider myself a person who works out regularly.

Apple’s Fitness challenges along with their recently released Fitness Plus service have played a huge part in my progress by not only motivating me to be more active but also making it easy to fit exercise in throughout the day even if it’s 10 minutes at a time.

In many ways, 2020 was not the year I expected it to be, as I’m sure was the case for many. Many of my goals had to be postponed (like our wedding) or abandoned entirely (reading) in order to just maintain sanity. Other goals seemingly appeared out of nowhere and exceeded my wildest expectations, but as we come out 2020 and move into 2021, it’s clear to me that my life has changed for the positive despite all the obstacles that were put in front of me.

That’s why for 2021, my focus is progress.

The incremental changes I made for my health have become an ongoing area of focus that I hope to continue making progress.

Another area I made huge strides in last year was my finances, which I expect will be the biggest area of progress for the year. I’m already working on refinancing my condo to a better rate, and after becoming debt-free other than the mortgage last year, I’m now working towards financial independence.

The reason for my dabbling was due to a feeling of uneasiness when using Evernote. For years, I’ve been increasingly less and less confident in the Evernote’s future or the company’s values, but in the absence of no better alternative, I stuck around hoping the tides would turn.

Suffice to say, the tides haven’t turned, and their recent app updates removed several of my most used features. Sure, Evernote keeps saying that they’ll bring these features back in the future, but this is also the same Evernote who said the new versions would be better than ever. Spoiler alert: They’re not.

One thing that has changed, however, is the world of Evernote competitors. It’s hard to say there are no better alternatives anymore, especially now that my needs have simplified, which is why I started thinking about what I truly needed out of a personal knowledge management system.

Topping the list of must-need features:

I need to be able to save important emails easily for reference.

I need to be able to add multiple file types.

I need to be able to link to notes both within and outside of the system.

My obvious first choice would have been Apple Notes, which I’m already using for sharing notes with my other half. Unfortunately, while it does meet most of my needs, it doesn’t have any sort of integration with my email app. Note links are also quite clunky. You pretty much have to pretend to share the note with someone to get a note link.

The highly-praised Notion was next on my list, but quite honestly I don’t have the patience to set up a database from scratch.

I also tried OneNote, but, my gosh, the interface is “oh-so-Microsoft Office” and seemed way too fiddly for my needs. No thank you.

At this point, I’ve settled with Bear. I’m still getting used to the tag-based structure, but overall, I’ve been liking it a lot more than I expected. This is in part to the simplification of my organizational needs from when I last tried it. There are a few things I do miss, like tables, but those seem to be on the road map so hopefully, the wait won’t be too terribly long. It’s also worth mentioning that Bear’s Pro subscription is around 20% of what a year of Evernote Premium would cost me.

With that said, I really do hope the best for Evernote. As a note-taking service, it’s still a pretty great option for most users, I’m just not sure I’m most users anymore. If they can prove me wrong, I’m still keeping my options open, but for now Bear seems to be my best bet.